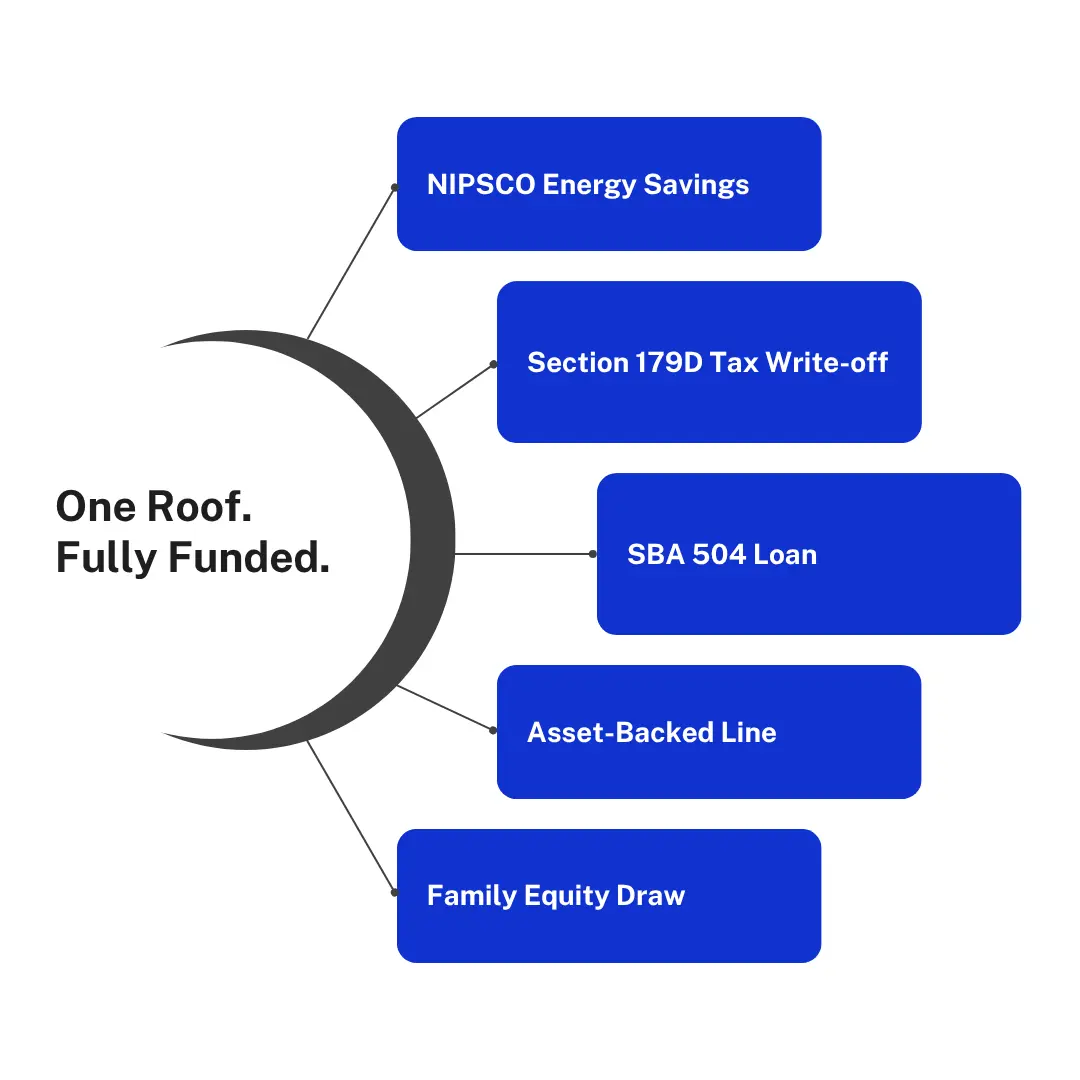

"He owns six businesses. Even one asset positioned right unlocks the rest."

A building owner came to us convinced he could not qualify. His cash flow had taken a hit. His personal FICO was not where he wanted it. He had already heard discouraging news from a conventional lender.

What nobody had done yet was look at the full picture.

He owns six businesses. Some are doing well. Some are lean. But across that portfolio — the equity, the ownership stakes, the real property — there was more than enough for a lender to feel safe against.

Creative capital does not come from one source. It comes from looking at everything you have already built and asking which piece can move first.

One asset, positioned correctly, unlocked the rest.